The real open finance advantage for banks? Monetising APIs.

May 23, 2021 | News

Imagine having cash-flow predictive analytics that you could share with others. Now imagine that you could offer a loan on the end of those analytics and let it go into the market. Sounds simple, right? But one still largely unexplored way for banks to capitalise on open finance is to build and monetise next-level APIs where it makes sense to. There’s great value in data sharing, both for the ones sharing data and for the banks, so why not monetise the data exchange itself and start building an economy around the APIs?

Aiia CEO Rune Mai believes that this is the next logical step and real advantage to open banking’s evolution into open finance. He recently sat in on a MoneyLive Digital Summit panel discussion together with Hetal Popat, Director of Open Banking at HSBC Group. They had a lively chat about the future of open finance and how banks can harness its opportunities and pass them along to consumers. Here are some key takeaways from the conversation:

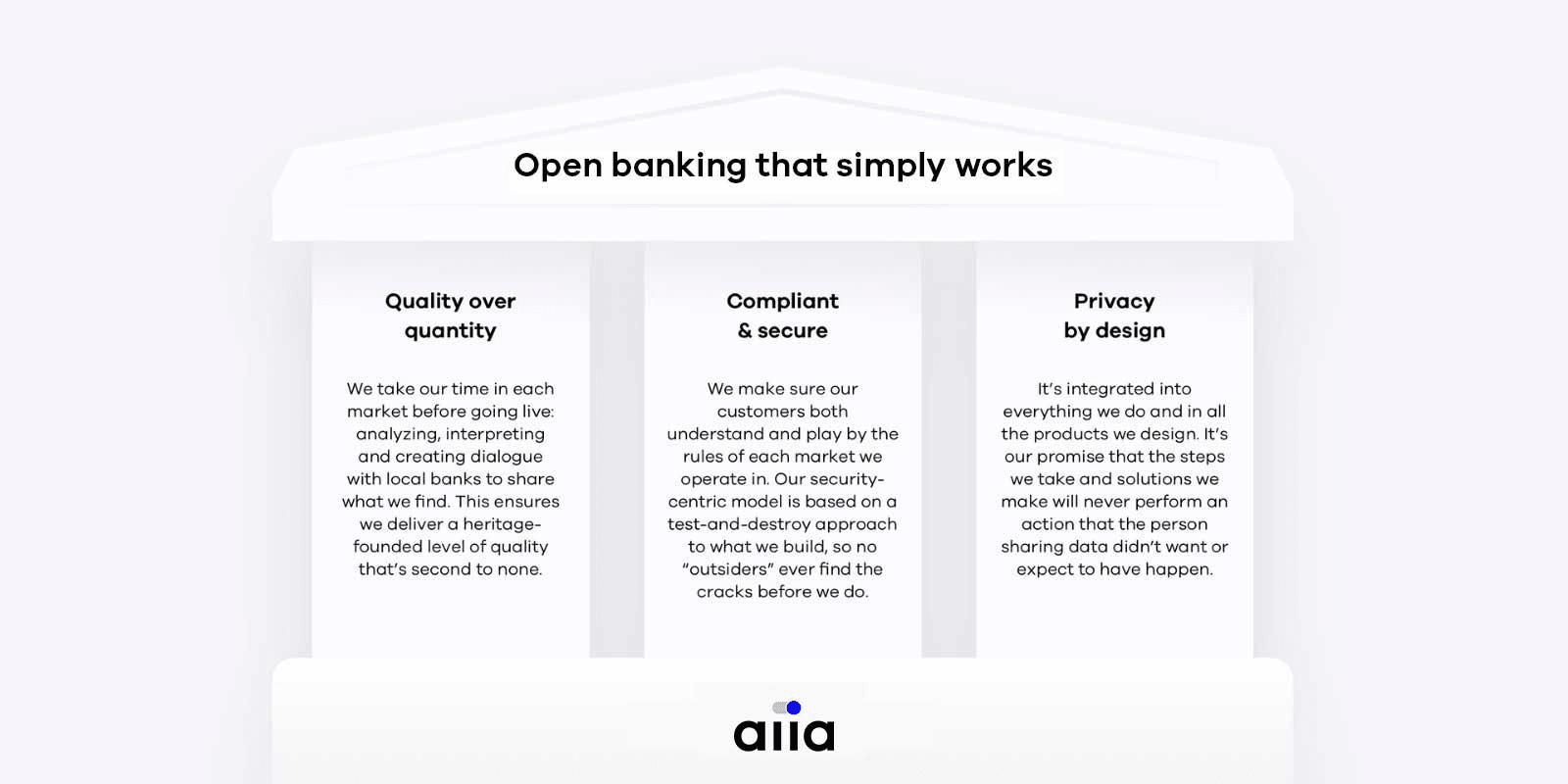

First off, can you explain what you mean when you say Aiia is “open banking that actually works”?

Well, it’s really hard to build quality into open banking. At Aiia, we focus on three principle “pillars” - quality over quantity, complaint and secure, and privacy by design - that we believe are missing when it comes to some of the solutions currently being offered on the market.

It’s becoming increasingly important to get these pillars right in order to nurture increased consumer adoption. We spend a lot of time focusing on them and it shows; we have 95% payment and data coverage in the markets we operate in, and prominent names such as Danske Bank, Santander, DNB, OP Bank and neobank Lunar who trust us to take their open banking efforts to the next level.

We’re currently rolling out our model to the rest of Europe and expect to be fully pan-European by the end of this year.

What does the term “open finance” mean to you?

Open finance is a broad term that encompasses a lot of various industries. In the end, open finance is about value exchange and being able to follow that exchange in more automatic, convenient ways that will help us in the future.

In more specific context, open finance is what allows banks to undergo digital transformation - to move from a branch-oriented to a product-oriented focus - so they can meet customers wherever they are, whenever they want to. Moving from “branch to build” goes way beyond what we expect from banks today. It allows them to start building ecosystems around themselves that in turn create markets.

So is open finance the next logical step for open banking?

Totally. It makes so much sense. However, open banking has been “forced” upon banks. It’s not like banks don’t benefit from open banking, but still, they have to provide a service - extending their own payment capabilities so others can consume it for free, for instance. It’s all a bit strange to be honest.

But banks have a real advantage when it comes to open banking, and open finance for that matter. There are great opportunities for banks to start monetising APIs and building themselves into other services. That’s where it becomes really interesting.

We see players like HSBC already taking advantage of this by monetising the payments front and situating themselves on top of the value chain instead of being tucked away somewhere below card infrastructures.

Can you give a specific example of how banks could benefit from moving to an open finance structure?

There are a couple of ways that banks can benefit directly from this move. One still largely unexplored way is to build next-level APIs for banks to monetise where it makes sense to. There’s great value in data sharing, both for the one sharing data and for the bank, so why not monetise the data exchange itself and start building an economy around the APIs? Imagine having cash-flow predictive analytics that you could share with others. You could then put a loan on the end of it and let go into the market. This would be a huge opportunity for banks because it would be their loan offering powering that solution.

Another way to benefit is in how you build the solutions. All that matters in the end is that the solutions built on top of the APIs are trustworthy, engaging and benefit-driven for the user. If that criteria isn’t met, people simply won’t use it. So building and maturing the right solutions - focusing more on user experience than functionality, for example - goes hand-in-hand with an uptake in user adoption.

What should banks be looking for in an open finance partner?

On one side of the spectrum you’d be looking for a partner to provide better services for your customers. On the other side, it’s banks looking for a partner who can help them with market distribution. Fintechs that generate distribution really fast are also a platform for others to engage with. So, as a bank, if you can act as the lending mechanism behind that platform or provide the account from where payments are made, then all of a sudden you’ve just multiplied your company goals by being part of a greater ecosystem than what you can build yourself. You can start co-creating services that you want to sell to customers or even non-customers for that matter.

Are other industries ready for open finance?

Many industries are consuming bank APIs to produce advantages in their fields. Pension companies are performing top ups to account payments to save on credit card fees and inconvenient bank transfers. Other industries are also performing KYC and onboarding more swiftly by using data from accounts.

On the other hand, many industries are still protective of the data they sit on for many reasons. But in the end, the realisation will be the same; it pays to open up because that’s what customers expect.

What kind of cross-industry partnerships are there that've embraced and capitalised on the open finance concept?

The partnership of banks teaming up with accounting systems providers yields a lot of impressive results, both in collaboration and competition. Now accounting system providers can adopt much of the banking parts and thus act as the primary interface for the bank customers. We’ve seen Danish-based accountancy software provider Ageras Group recently procure a large amount of investment capital to build a new bank. On the other hand, we see many banks buying up accounting system providers in order to present better solutions for their customers and non-customers alike.

In the Nordics, we see more and more retailers teaming up with banks to provide SCA-less (strong customer authentication-less) payments done directly from an account. This is an app-based payment that can be initiated directly from your bank account. These players are moving really fast and we’ll most likely see more of it happen, especially centred around payments.

What roles do regulators play in driving open finance forward?

Active participation from local FSAs is the most important part in delivering a sturdy setup with high quality everywhere. We’re fortunate to have had the latest EBA opinion align with that sentiment - that FSAs should be much more active in evolving open banking, and therefore open finance, at the local level.

Before this EBA push, FSAs were just trying to be compliant with EU regulations. Now the EBA has put forward supervisory actions for FSAs to take in order to ensure quality and remove obstacles. They’re even encouraging local FSAs to discipline banks that aren’t compliant. The bottom line is that the industry needs to be a part of the growth. It doesn’t come from regulation alone. You can’t regulate innovation.

If you want to watch the discussion online, simply sign up for free to MoneyLive TV and check out the fireside chat in Episode 3: The Journey to Open Finance. You can also reach out to our team to find out how we can help you power your solution to create more user-driven services based on open finance. Or head over to our open banking blog for more inspirational use cases and trends.