What is payment initiation and how can you use it?

August 14, 2020 | Louise Basse

Big changes are taking place in the payment landscape as new legislation and technology challenge the way we integrate payments into products and services. With the rise of contactless payments, there’s no doubt that payment initiation has become a global trend that’s here to stay.

But how does it actually work? And what businesses are able to benefit from the opportunities that payment initiation brings?

Take a look below to get a better understanding of what payment initiation is and how you can easily integrate it into your business.

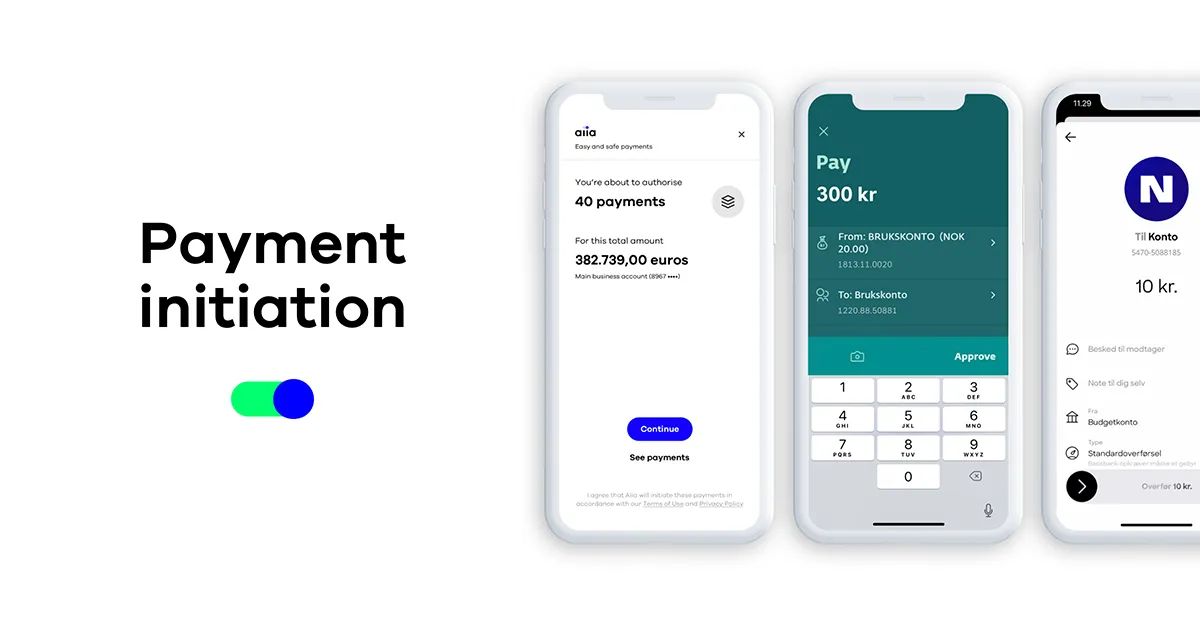

Payment initiation in a nutshell

Put simply, payment initiation is a payment method that enables you to integrate account-to-account payments directly into your service or product. By doing that, businesses are able to unlock a range of time-efficient and cost-effective benefits for businesses and consumers.

Payment initiation allows businesses to place all payment functionality from the online bank in the service or product they’re offering. In this way, consumers can skip the extra steps of changing context to initiate a payment.

Anyone with a bank account can pay and accept payments. Therefore, it’s safe to say that the potential use cases with payment initiation are practically endless – whether you’re shopping for new clothes online or paying invoices in an accounting system.

Here's a list of some of our customers that are using our payment initiation platform to create seamless payment options for their customers:

The benefits of account-to-account payments

But what are the actual advantages of using payment initiation and account-to-account payments? And how does it differ from traditional card payments?

According to Michael Juul Andersen, Chief Business Development Officer at Aiia, it’s all about convenience:

"Account-to-account payments are fast, inexpensive and virtually hands free. You can view your balance before confirming a payment while enjoying the same level of security a bank offers. It's no wonder why more and more credit card companies are tapping into the benefits of account-to-account payments."

Besides the obvious advantages of a clean, quick and cheap solution, account-to-account payments provide a reduction in fraud thanks to strong customer authentication (SCA) applied to each transaction, deliver instant refunds and dispense faster settlements.

See how open banking is changing the payments landscape

So, how does it work? And what are the use cases?

Because of the frictionless payment flow, account-to-account payments are designed for high conversion. To initiate a payment with our platform, you have to follow three simple steps:

- Request a payment by defining the amount and the receiver of the payment

- We send you a payment link that you need to present to your customer. We take care of everything in regards to the bank.

- Once the payment has been authorised in the bank, your customer will be returned to you when the payment is completed.

As we’ve previously emphasised, the potential use cases with payment initiation and account-to-account payments are practically endless. To mentioned a few, we’ve created a small list of businesses and industries that can benefit from using payment initiation to send and/or receive payments:

- Accounting software providers to do e-invoicing, bulk payments and more

- Banks to enable customers to move funds from other banks via another banks’ interface

- Payment gateways and the ecommerce space to offer better and more competitive payment options.

Want to learn more about the many payment opportunities available through open banking? Download our latest payment report or visit our open banking knowledge hub for more inspiration.